Sweepstakes casino winnings are taxable income. This surprises some players who assume that because sweepstakes casinos aren’t technically gambling, their prizes somehow escape IRS attention. They don’t. Every dollar you redeem from Sweeps Coins counts as income, and the IRS expects its share.

The critical distinction isn’t whether you pay taxes—you do—but how those taxes are categorized. Sweepstakes winnings get taxed as prize income, not gambling winnings. That single classification difference changes which tax form you receive, which deductions you can claim, and how much flexibility you have at filing time. “When it comes to sweepstakes casinos and their tax obligations, ‘different’ or ‘unregulated’ doesn’t necessarily mean ‘zero’ or ‘not paying taxes,'” noted Robert Stoddard, Partner in KPMG’s Tax practice, in the firm’s Sweepstakes Gaming Industry Primer.

The taxation framework matters more as the sweepstakes industry scales. With billions of dollars flowing through sweepstakes platforms annually—and individual players potentially redeeming thousands in prizes—the tax implications are no longer theoretical for a growing number of Americans. Getting it right protects you from penalties; getting it wrong creates problems that compound with interest.

This guide covers everything you need to understand about sweepstakes casino taxation: the forms involved, the reporting thresholds, the deduction rules that differ from traditional gambling, and the step-by-step process for filing correctly. The stakes are real—failure to report income can trigger penalties, interest, and IRS scrutiny you’d rather avoid.

1099-MISC vs W-2G: Why the Form Matters

When you win at a traditional casino—slots, poker, blackjack—and your winnings exceed certain thresholds, you receive a W-2G. This form is specifically designed for gambling winnings. It triggers specific tax rules, including the ability to deduct gambling losses against gambling winnings on Schedule A.

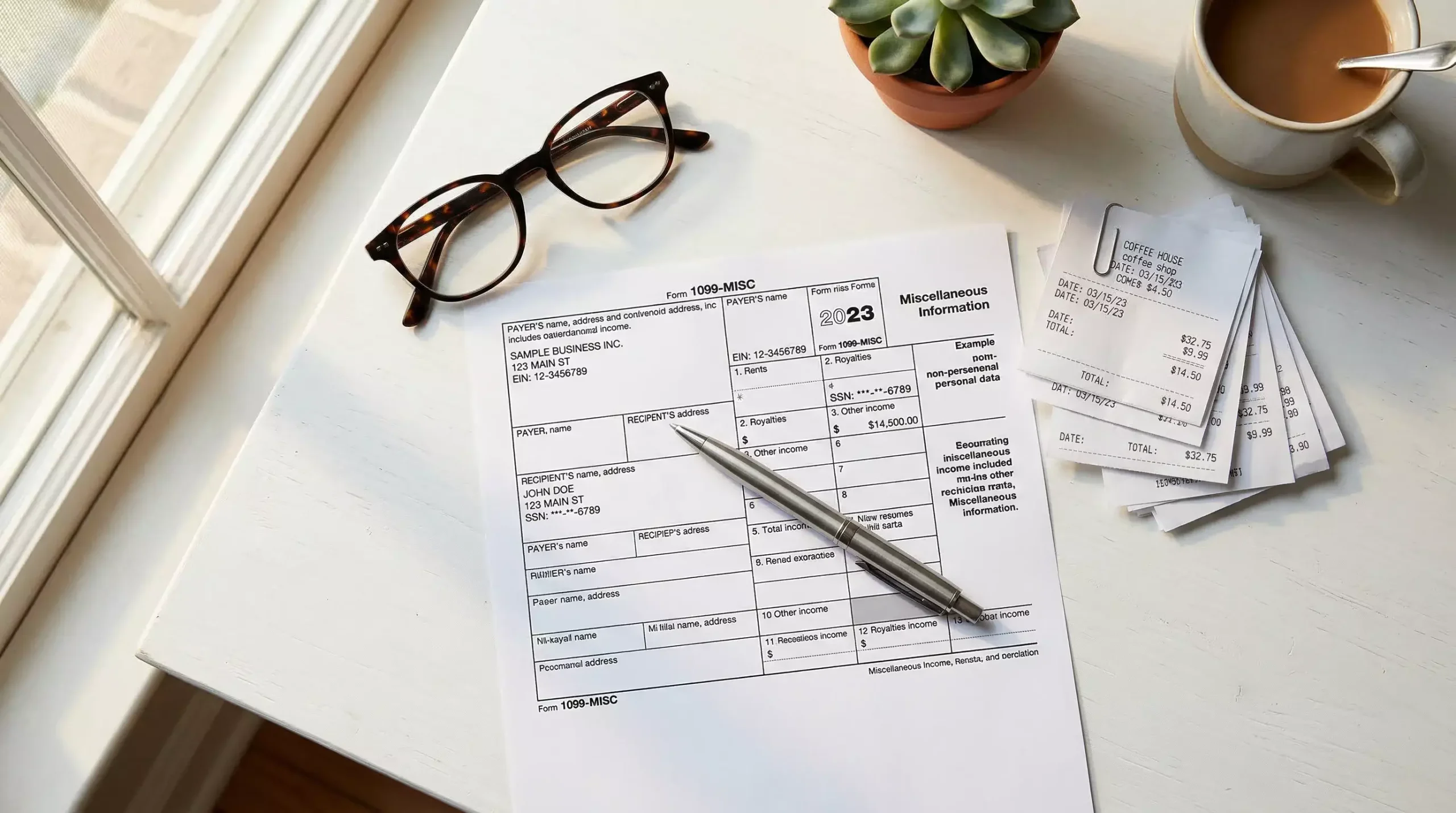

Sweepstakes casino prizes don’t use the W-2G. Instead, platforms issue 1099-MISC forms, categorizing your redemptions as prize income rather than gambling winnings. According to Sweepsy’s tax guidance, this distinction reflects the IRS’s classification of sweepstakes payouts as promotional prizes—the same category as winning a car in a raffle or cash in a corporate giveaway.

The scale of W-2G reporting gives context to the gambling industry’s tax infrastructure. Over 31 million W-2G forms were filed with the IRS in 2024, according to Tax1099’s analysis—a 29% increase from 2023. This represents the mature, regulated gambling industry’s reporting compliance. Sweepstakes casinos operate outside this established framework, using the separate 1099-MISC pathway.

The practical consequence of receiving 1099-MISC instead of W-2G centers on deductions. With a W-2G and traditional gambling, you can itemize gambling losses and deduct them against your gambling winnings, reducing your taxable gambling income potentially to zero (though not below zero—losses can only offset wins, not create deductions against other income). With 1099-MISC prize income from sweepstakes, no equivalent deduction mechanism exists for your Gold Coin purchases.

This isn’t an oversight or a loophole working against players. It reflects the legal structure sweepstakes casinos rely upon. If sweepstakes platforms issued W-2G forms, they’d be acknowledging their payouts are gambling winnings—undermining the entire legal argument that sweepstakes aren’t gambling. The 1099-MISC categorization is consistent with the promotional sweepstakes model, even though it creates less favorable tax treatment for players who spend significantly on Gold Coins.

Both forms ultimately report income that gets included in your gross income and taxed at your ordinary income rate. The difference is what you can deduct against that income before calculating your tax bill.

Understanding this form distinction helps set realistic expectations. Players transitioning from traditional online casinos in New Jersey or Pennsylvania to sweepstakes casinos in other states may expect similar tax treatment. The treatment differs meaningfully, and the difference favors the traditional gambling model from a pure tax perspective—though access considerations often outweigh tax optimization for players in states without legal iGaming.

Reporting Thresholds

Multiple thresholds govern sweepstakes tax reporting, and understanding each prevents surprises at tax time.

The $600 threshold triggers platform reporting. When you redeem $600 or more in Sweeps Coins during a calendar year, the sweepstakes platform must issue you a 1099-MISC form and file a copy with the IRS. This is cumulative across all your redemptions for the year—not per transaction. Redeem $300 in March and $350 in October, and you’ve crossed the threshold.

The $5,000 threshold triggers withholding. According to IRS Instructions for Forms W-2G and 5754, prizes exceeding $5,000 require 24% federal income tax withholding at the time of payment. This means the platform sends you 76% of your redemption amount, with the remaining 24% going directly to the IRS as prepaid tax. You’ll reconcile this withholding when you file your annual return—owing more if your effective tax rate exceeds 24%, or receiving a refund if it’s lower.

Starting in 2026, the reporting threshold increases to $2,000 under provisions of recent federal legislation. According to Sweepsy’s tax analysis, the “One Big Beautiful Bill Act” raises the 1099-MISC threshold, meaning players will receive fewer automated tax forms from platforms. This doesn’t change your tax obligation—winnings below $2,000 remain taxable—but it shifts recordkeeping responsibility more fully to the player.

Here’s the critical point many players miss: your obligation to report income doesn’t depend on receiving a tax form. The IRS requires you to report all taxable income, regardless of whether a 1099-MISC arrives. If you redeem $500 in Sweeps Coins, you won’t receive a 1099-MISC, but that $500 is still taxable income that should appear on your return. The form is an administrative convenience and audit trail, not the source of your tax obligation.

Platforms maintain records of all redemptions, and the IRS can request these records during audits. Failing to report sweepstakes winnings because you didn’t receive a form is a risk that rarely pays off and can result in penalties when caught.

Multiple redemptions from different platforms complicate tracking. If you play at Chumba Casino, WOW Vegas, and Pulsz, each platform tracks your redemptions independently. You might receive 1099-MISC forms from two platforms and not the third. Your total income across all platforms determines your actual tax obligation—not what any single platform reports. Maintaining your own comprehensive records across all sweepstakes activity is the only way to ensure accurate filing.

Can You Deduct Gold Coin Purchases?

The short answer: no. Gold Coin purchases cannot be deducted against sweepstakes winnings. This represents one of the most significant tax disadvantages of sweepstakes casinos compared to traditional gambling.

At a real-money casino, you can deduct gambling losses up to the amount of your gambling winnings. Win $10,000 at poker but lose $8,000 at slots during the year? Your net gambling income is $2,000, and that’s what you pay tax on (assuming you itemize deductions). The losses offset the wins.

Sweepstakes don’t work this way. According to IRS guidance as interpreted by Sweepsy, Gold Coin purchases are not gambling wagers—they’re purchases of entertainment products. When you buy a $20 Gold Coin package, you’re buying virtual entertainment credits, not making a bet. The fact that Sweeps Coins come along as a promotional bonus doesn’t transform the purchase into a deductible gambling expense.

The implications compound for players who spend significantly on Gold Coins. Consider a player who purchases $5,000 in Gold Coins over a year and redeems $4,000 in Sweeps Coins. At a traditional casino, this would represent a $1,000 gambling loss—no tax owed. At a sweepstakes casino, the player has $4,000 in taxable prize income and $5,000 in non-deductible entertainment purchases. The $5,000 spent is simply gone from a tax perspective.

This asymmetry is baked into the sweepstakes model’s legal structure. The argument that sweepstakes aren’t gambling depends on Gold Coin purchases being entertainment transactions, not wagers. If those purchases were deductible as gambling losses, they’d need to be classified as gambling expenses—contradicting the foundation of sweepstakes legality.

Some players explore whether Gold Coin purchases could qualify as hobby expenses or business expenses. Generally, no. Hobby expense deductions were effectively eliminated for most taxpayers under the Tax Cuts and Jobs Act of 2017. Business expense treatment would require demonstrating that sweepstakes play constitutes a business activity—a high bar that recreational players cannot meet.

The practical lesson: track your Gold Coin purchases anyway. While they’re not currently deductible, tax law changes, and having records protects you if future legislation creates new treatment options. More immediately, tracking purchases helps you understand your actual financial position beyond what tax forms show.

Federal and State Tax Obligations

Sweepstakes winnings face taxation at both federal and state levels, with rates varying based on your total income and where you live.

Federal income tax applies your marginal rate to sweepstakes prize income. For 2026, federal brackets range from 10% to 37% depending on your total taxable income. A player in the 22% bracket pays $220 federal tax on each $1,000 in sweepstakes redemptions. A player in the 32% bracket pays $320 on the same $1,000. Your sweepstakes income adds to all other income sources when determining your bracket.

State income tax adds another layer in most states. California taxes income up to 13.3% at the highest bracket. New York reaches 10.9%. Other states have flat rates or lower progressive scales. The combined federal and state bite can exceed 50% for high-income players in high-tax states.

Some states offer relief. Texas, Florida, Nevada, Wyoming, Washington, South Dakota, and Alaska have no state income tax. Tennessee and New Hampshire tax only investment income, not prize income. Players in these states pay federal tax only on sweepstakes winnings—a meaningful advantage.

Here’s a concrete example. A Texas player in the 24% federal bracket who redeems $5,000 in Sweeps Coins owes approximately $1,200 in federal income tax. The same player in California, in the same federal bracket but also facing California’s 9.3% rate (for income in that range), owes roughly $1,200 federal plus $465 state—$1,665 total. Same winnings, $465 difference based solely on state residence.

Self-employment tax does not apply to sweepstakes winnings for recreational players. Prize income is passive—you’re not performing services or running a business. This distinguishes sweepstakes taxation from, say, freelance income, where the 15.3% self-employment tax adds substantially to the federal burden.

The 24% withholding threshold at $5,000 doesn’t distinguish between state tax situations. If withholding applies, you’ll need to account for your actual state liability separately. States don’t typically require withholding on prize income the way they do on wages, so estimated tax payments may be necessary for large redemptions.

Local taxes add another potential layer. Some cities and municipalities levy income taxes independent of state taxes. New York City residents, for example, face city income tax in addition to New York State and federal taxes. Ohio cities commonly assess local income taxes. These local obligations apply to sweepstakes income just as they do to wages and other income. Check your specific locality’s tax requirements or consult a local tax professional.

The timing of redemptions can create state tax complexity for players who move during the year. Generally, states tax income earned while you were a resident of that state. If you relocate from California to Texas mid-year, sweepstakes income earned while in California remains subject to California tax. Accurate records of when redemptions occurred matters for players who change residence.

Record Keeping Requirements

Good records protect you during audits and simplify tax preparation. Here’s what to track and retain.

Redemption history is essential. Document every Sweeps Coin redemption: date, amount, platform, and payment method. Most platforms provide transaction history in your account dashboard—screenshot or export these records at least quarterly. Don’t rely on platform access remaining available indefinitely; operators can close, change systems, or restrict access to historical data.

1099-MISC forms require retention. When platforms issue these forms, keep copies for at least three years—the standard IRS audit window. Seven years provides extra protection if issues arise. Digital copies are acceptable; just ensure they’re backed up and accessible.

Gold Coin purchase receipts matter even though purchases aren’t deductible. First, they help you understand your actual profit or loss from sweepstakes play. Second, if tax law changes to allow some form of deduction, historical records become valuable. Third, in rare cases where sweepstakes activity might qualify as business income, documentation of expenses could become relevant. Keep credit card statements, platform purchase confirmations, and bank records showing Gold Coin transactions.

Track your basis for each redemption where possible. Some platforms show Sweeps Coin acquisition—whether from purchases, daily bonuses, mail-in requests, or promotions. While this granularity isn’t required for tax filing, it can help answer IRS questions if they arise.

Standard retention period: keep all sweepstakes-related tax records for at least seven years from the filing date of the return that includes that income. This covers the standard three-year audit window plus extensions that can apply in cases of substantial underreporting.

Filing Your Sweepstakes Winnings

The filing process for sweepstakes income follows a straightforward path, but the details matter.

Step one: gather your 1099-MISC forms. Platforms must mail these by January 31 for the prior tax year. If you haven’t received an expected form by mid-February, contact the platform directly. Remember that you may not receive a 1099-MISC if your total redemptions stayed below $600 (or $2,000 starting in 2026)—but you still owe tax on this income.

Step two: include the income on Form 1040. Sweepstakes prizes reported on 1099-MISC go on Schedule 1, Line 8z, as “Other Income.” You’ll write “Sweepstakes/Prize Income” as the description and enter the total amount. This flows to Form 1040, Line 8, combining with any other additional income.

Step three: account for withholding. If 24% withholding applied to any redemption over $5,000, the withheld amount appears on your 1099-MISC. This gets entered on Form 1040, Line 25b, as other withholding. The withheld tax counts as prepayment toward your annual liability.

Step four: calculate and pay any balance due. Your sweepstakes income, combined with all other income, determines your total tax liability. Subtract withholding (from sweepstakes and all other sources like wages). If you owe more, payment is due by the April filing deadline. If withholding exceeds your liability, you receive a refund.

For large redemptions or ongoing sweepstakes activity, estimated tax payments may be necessary. The IRS expects you to pay taxes as income is earned, not just at year-end. If your sweepstakes redemptions create a situation where withholding doesn’t cover your liability, and you expect to owe $1,000 or more when filing, estimated quarterly payments (due April 15, June 15, September 15, and January 15) can prevent underpayment penalties.

State filing follows similar logic. Include sweepstakes income on your state return according to that state’s instructions. Some states have separate schedules for prize income; others fold it into general income categories. State tax software or a tax professional can guide state-specific requirements.

Tax software handles most of this automatically if you enter your 1099-MISC information correctly. TurboTax, H&R Block, and similar platforms include interview questions that route prize income to the correct lines. Just ensure you categorize the income correctly—as prize income, not as self-employment or business income, which would trigger additional forms and potentially self-employment tax.

For players who prefer paper filing or who have complex situations, IRS Publication 525 (Taxable and Nontaxable Income) provides detailed guidance on prize income reporting. This publication clarifies which income is taxable, where to report it, and how it interacts with other income types.

Common Tax Mistakes to Avoid

Several errors appear repeatedly in sweepstakes tax situations. Avoiding them protects you from penalties and IRS attention.

Failing to report income below the 1099 threshold is the most common mistake. If you redeem $500 in Sweeps Coins and receive no 1099-MISC, you still owe tax on that $500. Many players assume “no form means no tax.” The IRS disagrees. When audits occur, platforms can provide complete redemption records that reveal unreported income. Penalties for unreported income include accuracy-related penalties (typically 20% of underpayment) plus interest.

Attempting to deduct Gold Coin purchases as gambling losses triggers problems. Some players, knowing that gambling losses are deductible against gambling winnings, try to apply the same logic to sweepstakes. This mischaracterizes the transaction and creates audit risk. If questioned, you’ll need to explain why you treated entertainment purchases as gambling losses—an explanation that undermines the sweepstakes model’s legal premise.

Ignoring state tax obligations creates liability. Players in states with income tax sometimes file federal returns correctly but neglect state requirements. States increasingly share data with each other and with the IRS. Cross-referencing 1099 forms against state returns is routine. Unreported state income eventually surfaces.

Misunderstanding withholding as final payment confuses some players. When 24% is withheld from a large redemption, that’s a prepayment, not necessarily your total tax bill. If your marginal rate exceeds 24% (plus state taxes), you’ll owe additional tax at filing time. Spending the full redemption amount without reserving funds for additional tax creates cash flow problems in April.

Discarding records too early limits your options. If the IRS questions your return three years later, having redemption histories, purchase records, and filed forms makes responses straightforward. Without records, you’re reconstructing from memory—a weak position.

The Bottom Line on Sweepstakes Taxes

Sweepstakes casino winnings are taxed as prize income, not gambling winnings. This classification determines which forms you receive, which deductions you cannot take, and how federal and state taxes apply. The IRS treats these prizes like any other income—subject to reporting, withholding at higher amounts, and full inclusion in your annual return.

The non-deductibility of Gold Coin purchases represents the most significant practical difference from traditional casino taxation. You cannot offset your winnings with your purchases, which makes the effective tax bite on net sweepstakes activity higher than on equivalent gambling activity. A player who spends $3,000 on Gold Coins and redeems $2,500 in Sweeps Coins has $2,500 in taxable income and $3,000 in unrecoverable costs—an unfavorable position that wouldn’t exist with W-2G treatment.

Good recordkeeping, timely filing, and accurate reporting protect you from penalties and audits. The rising 1099 threshold to $2,000 in 2026 shifts more responsibility to players for tracking and reporting income—platforms will issue fewer forms, but your tax obligations remain unchanged.

Planning ahead helps manage the tax burden. If you anticipate significant redemptions, consider timing—spreading redemptions across tax years might keep you in lower brackets. Understand your withholding situation before large redemptions so you’re not surprised by reduced payouts. Set aside tax reserves rather than spending full redemption amounts.

For players with significant sweepstakes income—thousands of dollars in annual redemptions—consulting a tax professional makes sense. CPAs familiar with prize income can optimize your filing approach, ensure compliance, and identify legitimate strategies that general guidance cannot provide.

This guide provides general tax information about sweepstakes casino winnings. It is not tax advice. Tax situations vary by individual circumstances. Consult a qualified tax professional for guidance on your specific situation. Information reflects tax law as of March 2026.